“It was the best of times, it was the worst of times…” Charles Dickens, A Tale of Two Cities

Charles Dickens is one of history’s most accomplished authors, best known for A Christmas Carol, Oliver Twist, David Copperfield and of course, A Tale of Two Cities. A Tale of Two Cities tells the story of the hardships of peasants during the French revolutionary period in the late 1700s. The opening sentence of this literary classic is one of the most recognizable in all literature, and at the moment it happens to appropriately capture the stark contrast between the severely-damaged economy and the high-flying stock market.

The sharp rebound in stocks has been one of the most surprising in decades. It’s happened in the midst of record unemployment numbers and the worst contraction in GDP in more than 70 years. If investors sometimes need to be reminded that economic growth and stock-market performance aren’t always in lockstep, 2020 is thus far the quintessential case study.

But how is it possible that “the market” is actually higher than it was on December 31, 2019, which in retrospect seem like simpler times, when unemployment was at a record low and the economy was humming along?

Before digging into the details, we must first define “the market.” To many people the market refers to the most widely-followed indices: the Dow Jones Industrial Average, the S&P 500 Index, or the NASDAQ. Each has its own attributes, but for the purposes of this article we’ll refer to the S&P 500, which contains 500 of the largest publicly-traded U.S. companies as measured by market capitalization (total value of the equity of the company).

2020 Market Returns: What’s Under the Hood?

The “Tale of Two Markets” is an apt description of the S&P 500 itself because of the top-heavy nature of the underlying stocks in this index. As of this writing, the top five stocks in the index (or 1% of the total number of companies) are Apple, Microsoft, Amazon, Facebook and Alphabet (aka Google). These five companies alone comprise almost 22% of the total value of the index.

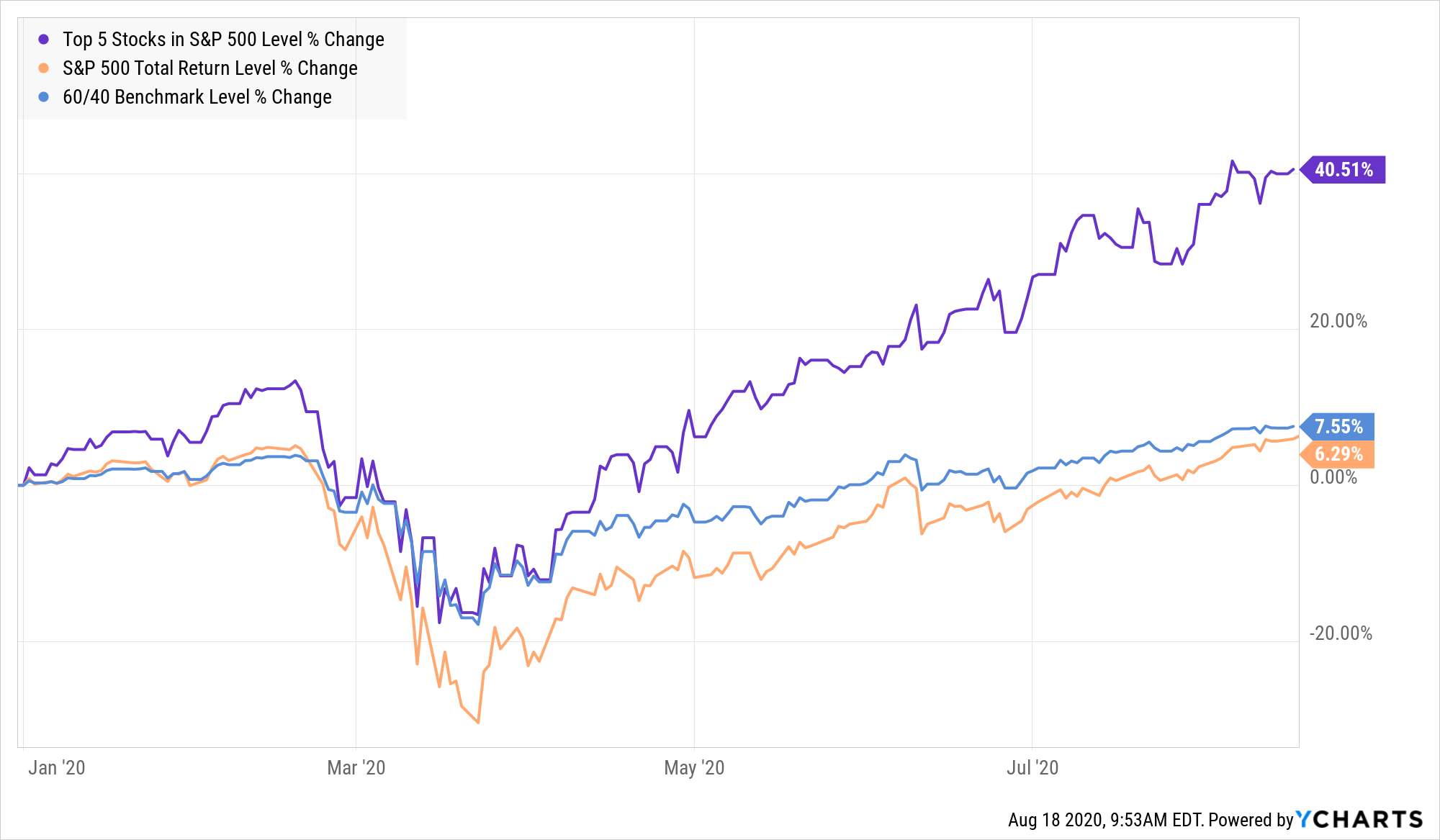

As shown below, the year-to-date total return of these five stocks (equally-weighted) far outpaces the broader index, let alone a traditional balanced portfolio that includes bonds. Their strong performance is the main reason the index overall recovered so well. The technology sector overall has also grown to a historically-large portion of the index. It currently represents about 27% of the market weight.

The potential problem with this dynamic is that history is not kind to these top performers. Over the last thirty years or so, stocks that grew to represent more than 3% of the index went on to underperform the broader index over the next one-year, two-year, and three-year periods. In today’s world, that would qualify four of the top five, excluding Facebook. Trends like this unwind eventually. This time could certainly be different, but it’s risky to pretend this could continue forever.

The scale and speed of government intervention to support markets has been, to overuse the adjective, historic. The federal government’s stimulus packages and the Federal Reserve’s massive liquidity injections have helped restore confidence in the markets. These policies put money in consumers’ pockets, kept interest rates at historic lows, and for the first time ever provided a buyer of last resort for corporate debt. The combination of all these policies was the ultimate put option, providing investors with confidence that governments would intervene to mitigate the damage from severe market disruptions. This has fueled speculative investing and has encouraged more risk taking and retail investor enthusiasm for stocks that are familiar and popular.

This doesn’t necessarily argue that investors should immediately sell these stocks altogether. These companies have not only survived but thrived in the midst of the pandemic. They have benefited from the acceleration of e-commerce and remote work, which were already gaining steam. Clearly these are fantastic companies with healthy profits, strong competitive advantages, and war chests of cash. Still, it does make sense to monitor their relative weight in the portfolio, as well as the valuation, quality, profitability, and growth prospects of each.

Implications for Investors – Now What?

In light of all this, a well-defined portfolio strategy tailored to actual cash flow needs is absolutely critical to navigate these stormy waters.

- Given higher valuations and the top-heavy nature of the index, it’s wise to temper expectations for future growth. Using conservative growth estimates in financial planning helps maximize the probability of achieving goals and prevents the need for painful adjustments down the road.

- Investors should also keep in mind that today’s stock market heroes tend to underperform in the future, as noted above. This means diversification across asset classes, sectors, and geography is critical to maximize the chance of investment success. In the long run it pays to avoid the drift of momentum trades and overexposure to any one company, industry, or sector.

- As always, investors should protect themselves from stock-market volatility by holding enough bonds as well as a healthy cash cushion. It’s prudent to have enough invested in bonds to cover cash-flow needs for five years or more, depending on one’s risk tolerance. It’s also wise to keep enough cash on hand to fund several months or even up to a year of cash-flow needs. This can be a “drag” when stocks are rising, but this bucket of safe assets provides peace of mind to avoid panic selling when markets are in turmoil.

Find more practical advice on a wide variety of wealth management topics by exploring our JIC Blog: Beyond the Number library.

Published 08/18/2020

Johnson Investment Counsel cannot promise future results. Any performance expectations presented here should not be taken as any guarantee or other assurance as to future results. Our opinions are a reflection of our best judgment at the time this interview occurred, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise.