Barring a historic recovery in stock and bond markets in the coming days, the numbers, tables, charts, and graphs on upcoming mid-year investment reports will clearly define what all of us already know in our gut: this has been a rough first half of the year. Gallons of “ink” (actual and virtual) will be spilled to analyze, explain, diagnose, and detail all the reasons for the decline. There will be thousands of recommendations for short-term trades or shifts in asset allocation to put a tourniquet on the red ink spilling on investment statements.

Many of these suggested tactics are simple educated guesses, typically short sighted, and have a troubling propensity to inflict even more damage. Despite best intentions, there’s just no escaping the fact our brains are hardwired to “do something.” Even the most accomplished and most educated industry experts are not immune. Consider a recent Wall Street Journal article in which Bill Bengen, the inventor of the famed 4% rule of thumb, candidly admits that the current markets have him unnerved. The man who literally wrote the research that a person could safely withdraw 4% annually from the portfolio and not run out of money has succumbed to psychological pressures. He is modifying his asset allocation, going against his own research.

But can doing nothing be part of a good plan? Yes. The temptation is strong to be doing something when markets are moving, making short-term calls to “get out now” and “get in when things recover.” But there are endless studies and statistics that highlight the folly of attempting to time the market. Here are two of the most powerful for keeping proper perspective:

- One recent study highlighted the latest data on the impact of missing even a few of the market’s best days. Specifically, between 2002 and 2021, seven of the best ten days of market performance occurred within ten days of the worst days. In fact, six of the seven days occurred the very next day after the worst days. By missing the ten best days over 20 years (ten days out of 7,300) an investor would cut their annualized return nearly in half (from 9.5% to 5.3%).

- The research firm Dalbar published their annual report on average investor gains vs. S&P 500 gains. From 1992 through 2021, the average stock investor earned an annual return of 7.1%, versus the S&P 500 return of 10.7%. That 3.6% spread may not sound like much, but over several decades it can be life changing. Starting with $100,000 in 1992, this underperformance would have resulted in $789,456 compared to $2,082,296. This massive gap could mean the difference between retiring at age 60 instead of 65, having the ability to pay for college, or buying a vacation home.

Why did the average investor perform so poorly? Very simple – selling out of fear and locking in losses.

These metrics confirm a well-worn investing axiom: “if it’s painful, it’s probably the right decision.”

What to do instead? We employ another well-worn axiom that is easier said than done: “control what you can control and ignore the rest.” This means having both a mental framework and an actual plan already in place before the inevitable market volatility tempts us to react. Having a disciplined approach in place based on fundamental investment principles can provide priceless peace of mind.

Control What You Can Control

- Maintaining Adequate Reserves: A critical concept to define for a household is annual spending (including taxes) relative to the amount of safer assets like high-quality bonds and cash. While 2022 has been an anomaly for bonds, along with cash they act as a shield against poor and potentially irrevocable financial decisions. We know the stock market almost always rebounds to exceed prior highs within three to five years. That’s why we encourage clients to maintain several years of living expenses in these less volatile asset classes. This allows us to wait out the recovery and avoid locking in losses by selling stocks at or near the bottom.

- Execute on Timely Strategies: We can’t control markets, the Fed, tax policy, or investor sentiment, but we can utilize tactics that improve the after-tax results in a portfolio. We’ve written extensively on these topics and the links to these articles are provided, but in short, we suggest using these volatile times to make lemonade out of lemons.

- Tax Loss Harvesting: Realizing capital losses to deduct or offset other taxable income can be done without timing the markets. While caution is necessary to execute this properly, this is another way we use these volatile times to lower income tax liabilities and rebalance a portfolio in need of realignment. Details on how we approach this can be found in our blog Spring Cleaning the Portfolio.

- Keep Buying: If still employed, experience the magic of consistent deposits to retirement and taxable accounts via automatic contributions. When markets are in a tailspin, these automatic deposits lead to buying low without the angst of having to actively buy amid so much negative news. This disciplined process eliminates trying to make purchase decisions based on emotion, gut, or fear.

- Roth Conversions: We evaluate this strategy in any market environment, especially for recent retirees whose taxable income is now lower due to lack of income from work, and who have yet to collect Social Security or mandatory IRA distributions. Converting pre-tax dollars to Roth IRAs can set the stage for decades of tax-free growth when the inevitable recovery takes hold. For more detail see our article The Golden Window of Tax Planning.

Learn From History

It’s been said that the four most expensive words in investing are “this time is different.” This phrase is a criticism of those who believe that today’s troubling times are unique, history doesn’t matter, and markets will never recover. However, there are always ways that history repeats itself, and there are ways that every environment is unique. As a result we must be cognizant of the bedrock principles that eventually lay the groundwork for a recovery after even the most difficult periods.

These include our country’s free enterprise system, the creative genius of our innovators, contract law, and a relatively stable government. Wars, economic policies, natural disasters, and geopolitics lead many to question the viability of our system. Those questions grow during challenging times. During any period of turmoil the far more likely outcome is that the country and economy will heal and overcome these challenges, given enough time. The next time this doesn’t happen would be the first time in our history.

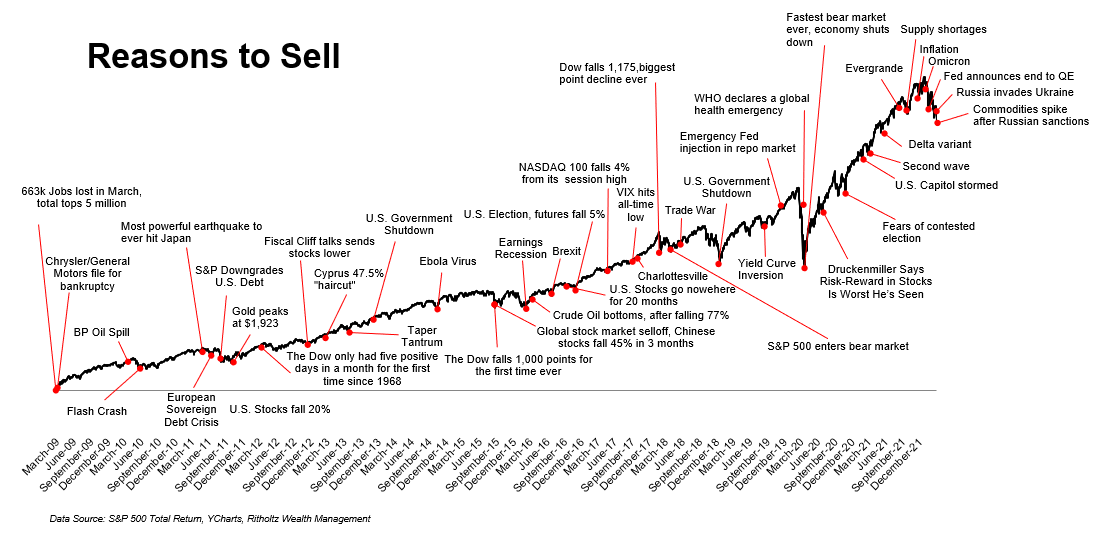

As noted in the chart below, we’ve faced many difficult times and there are always excuses to sell out and be “safe.” But as can be seen by the longer-term trajectory of the stock market, “safety” would have meant missing out on substantial returns. After today’s crises eventually pass, more are certain to come our way. This is a good reminder there is no “perfect” time to invest.

Bottom Line

Fear can be a powerful motivator. For most of human history, this has served well as a survival instinct. But short-term fearful reactions can be fatal to an investment plan. Patience and discipline are the principles most richly rewarded. Having a plan, controlling what we can control, and keeping a long-term perspective can allay these fears and serve as powerful immunity against panic selling. Avoiding this one critical error is a fundamental key to long-term financial success.

Published 06/21/2022

Johnson Investment Counsel, Inc. (“JIC”) is an independent and privately owned investment advisory firm registered with the Securities and Exchange Commission. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors prior to taking any action. Some of the comments, scores and probabilities in this presentation are based on current management expectations and are considered “forward-looking statements”. Actual future results, however may prove to be different from our expectations. Our opinions are a reflection of our best judgment at the time this presentation was created, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise. To determine if the strategy presented is appropriate for you, carefully consider the investment objectives, risk factors, and expenses before investing. Individual account management and construction will vary depending on each client’s investment needs and objectives.