Why We Recommend Focusing on Time in the Market vs. Timing the Market

For more reasons than we care to recount, 2020 will certainly go down as a year to remember and a year to forget. The prudent investor, however, can reflect on 2020 as a historic “teachable moment” on how counter-intuitive market performance can be and how attempting to time the market can be confounding, and even dangerous.

Recent headlines have highlighted how an increasing number of investors have treated the stock market more like a short-term gamble than a long-term savings strategy. A potent cocktail of gamified trading apps and media-driven hyperbole has drawn many new investors in, which has led to higher volatility in certain areas of the market. January’s “short squeeze” of Gamestop and other stocks showed just how far retail investing has come thanks to these technologies.

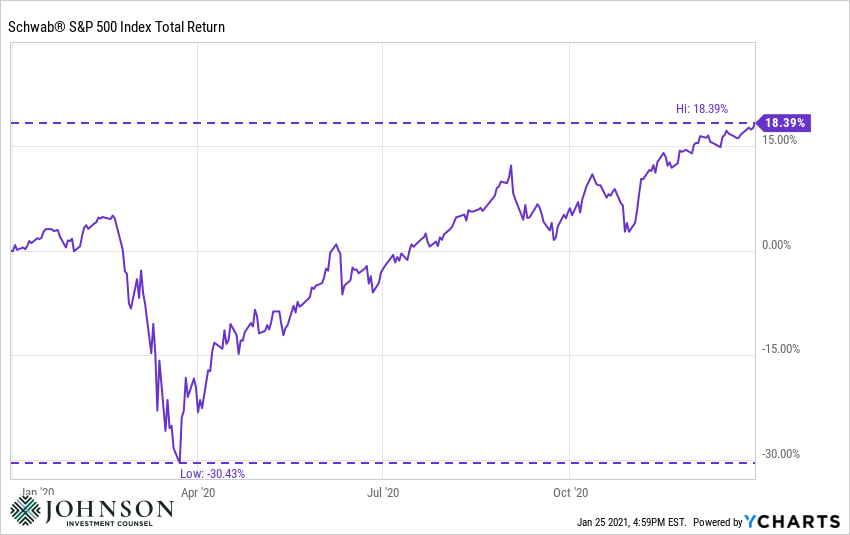

The chart below depicts just how volatile stock markets can be. The 2020 roller-coaster ride is a case study in both the severity and the speed of 30%+ market moves. What’s interesting is that many years from now when memory has faded, return tables of the S&P 500 will simply show an 18% gain - just another “above-average” year for stock investors.

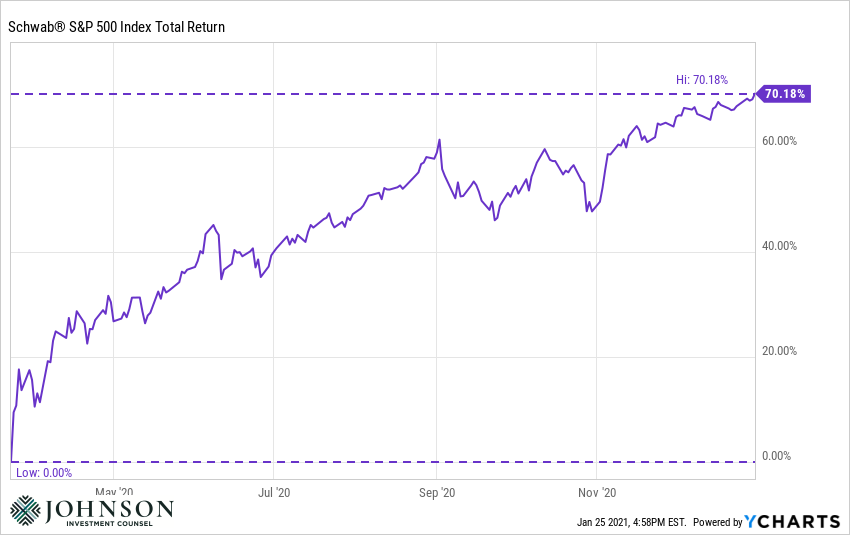

Looking back at the nadir of the S&P 500 on March 23rd, one couldn’t be blamed for considering selling stocks. Those who did were mostly thinking about the four most expensive words in investing: “It’s different this time.” To be fair, 2020 was different in that it’s been over 100 years since we’ve endured a global pandemic. But what was not different was that stock markets tend to overreact in the short term but typically course-correct over the long term in valuing the future value of companies’ cash flows. In fact, if one was horribly unfortunate and exited at the bottom of the market on March 23rd, they would have missed a 70%+ return from the bottom in just over nine months.

Of course, hindsight is 2020 (no pun intended) but the point is that protecting ourselves from ourselves is paramount when it comes to emotion-driven buying and selling. Too often investors project either irrational fear or over-confidence regarding future returns and in turn, buy or sell before they think “the market” will move higher or lower.

Studies Confirm Time in the Market Beats Timing the Market

Are You Prepared to Protect Yourself from a Knee-Jerk Reaction?

Unfortunately, numerous industry studies confirm the historic damage suffered by those succumbing to the siren’s song of market timing.

One study done every year by the research firm DALBAR Inc. details the 20-year history of the typical investor, the most recent spanning December 31st, 1999 to December 31st, 2019. The critical takeaway is that while the S&P 500 returned an average of 6.06% per year since 1999 (including two harsh bear markets in 2001 and 2008), the average stock investor only realized about 4.25% per year. While 1.81% may seem insignificant, over the course of 20 years the difference in dollars is nothing short of staggering. For reference, starting with a $500,000 portfolio at age 45, this emotion-led gap in returns year after year would compound to an account value of $1.1 million instead of $1.5 million, a shortfall of $400,000. In real life, that could mean extra years of early retirement or grandchildren’s college educations.

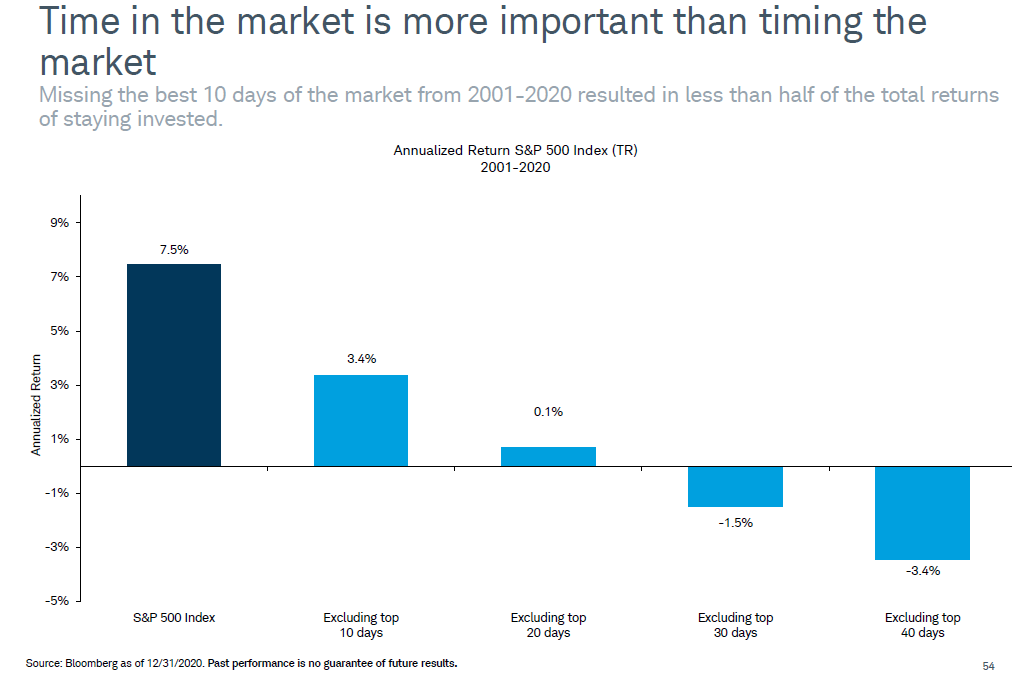

Even more striking is the impact of missing just a fraction of the market’s best days over the course of 20 years as noted by a study published by Charles Schwab in their 2021 Quarterly Chartbook (please see chart below). Using the S&P 500 as a proxy, this study clearly demonstrates the damage inflicted on returns by missing just a few days out of thousands of days over 20 years.

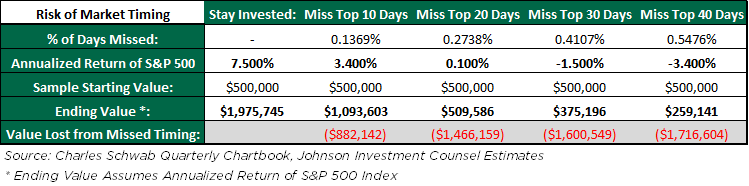

To put this in perspective, an investor who started with $500,000 and missed just 40 of the top days of market returns in 20 years (or about 0.5% of the days) would have missed out on $1.7 million! (Please see table below for additional detail.)

To add insult to injury, the investor would have likely spent endless hours researching their investment thesis and enduring countless sleepless nights trying to “make the call” on both when to get into the market and when to get out.

Knowing all this, how does an investor inoculate themselves from themselves? We would suggest two simple strategies:

- Calculate your bucket of safe assets: Calculate net living expenses (stable income less after-tax expenses) then design a portfolio allocation that ensures at least five years of net living expenses in cash and high-quality fixed income securities. Most bear markets last about three to four years before markets return to a new high, although it can take longer. By having this safe bucket of assets from which to pull without having to sell stocks, one can breathe a bit easier.

- Seek trusted & objective counsel: High-quality wealth advisors provide one thing that is impossible for people to provide for themselves, no matter how educated or how closely one studies markets and investing: an objective perspective. It is impossible for one to remain completely dispassionate and objective and therefore impossible NOT to get emotional about the ups and downs of the markets.

Like New Year’s Resolutions, investment strategies are undertaken with great intentions. The problem isn’t thinking of them, the problem is sticking with them in times of stress and when the short-term outlook is grim. Preventing a knee-jerk reaction when witnessing a sharply dropping (or sharply increasing) market is how investors can avoid big mistakes and their worst enemy: themselves.

Find more practical advice on a wide variety of wealth management topics by exploring our JIC Blog: Beyond the Numbers library.

Published 02/16/2021

Any expectations presented should not be taken as a guarantee or other assurance as to future results. Our opinions are a reflection of our best judgment at the time this presentation was created, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise. The material contained herein is based upon proprietary information and is provided purely for reference and as such is confidential and intended solely for those to whom it was provided by Johnson Investment Counsel.