When fortunate enough to have some rare downtime, some people spend a few minutes flipping through the endless cable channels hoping to come across a favorite movie. We all have that list of personal favorites we’ll stay up late and watch to the end regardless of where we pick up the story. For me, a few favorites are Gladiator, The Fugitive, Shawshank Redemption, and The Godfather (I and II, but certainly not III).

Another might be the 1971 classic Dirty Harry, starring Clint Eastwood. One of the more famous scenes reminds me of a common question we get from clients. Clint Eastwood says to a wounded criminal in his signature style “You have to ask yourself one question: Do I feel lucky? Well, do you, punk?” This is a great starting-point question for future retirees with pensions facing the big decision of whether to take a monthly payout or a lump sum rollover to an IRA.

And the Dirty Harry question to retirees is:

“Do you feel lucky (about your longevity)?”

While that may be a simple question, the analysis is actually quite complex as retirees must consider a number of factors beyond that in order to make the most informed decision. So let’s run through a list of questions and issues one must address.

Before we get to the questions we must start by estimating the annual “return” of the monthly pension payment and compare that to estimated market returns on a potential rollover to an IRA. This can be calculated by annualizing the monthly payment (for example, $2,500 per month x 12 = $30,000 per year) and dividing it by the lump-sum option. Assume the lump sum option is $750,000. $30,000 per year / $750,000 = 4%. Not a bad “income stream” return in today’s world of low interest rates, BUT we must evaluate many other factors while keeping this 4% in mind.

Next, we have to answer the “Dirty Harry Question,” followed by a series of other important questions. (DISCLAIMER: These questions are general guidelines only as every plan and every personal circumstance is unique. You should always consult your professional team of advisors to break down the details of your plan and your situation.)

So the Dirty Harry Question is:

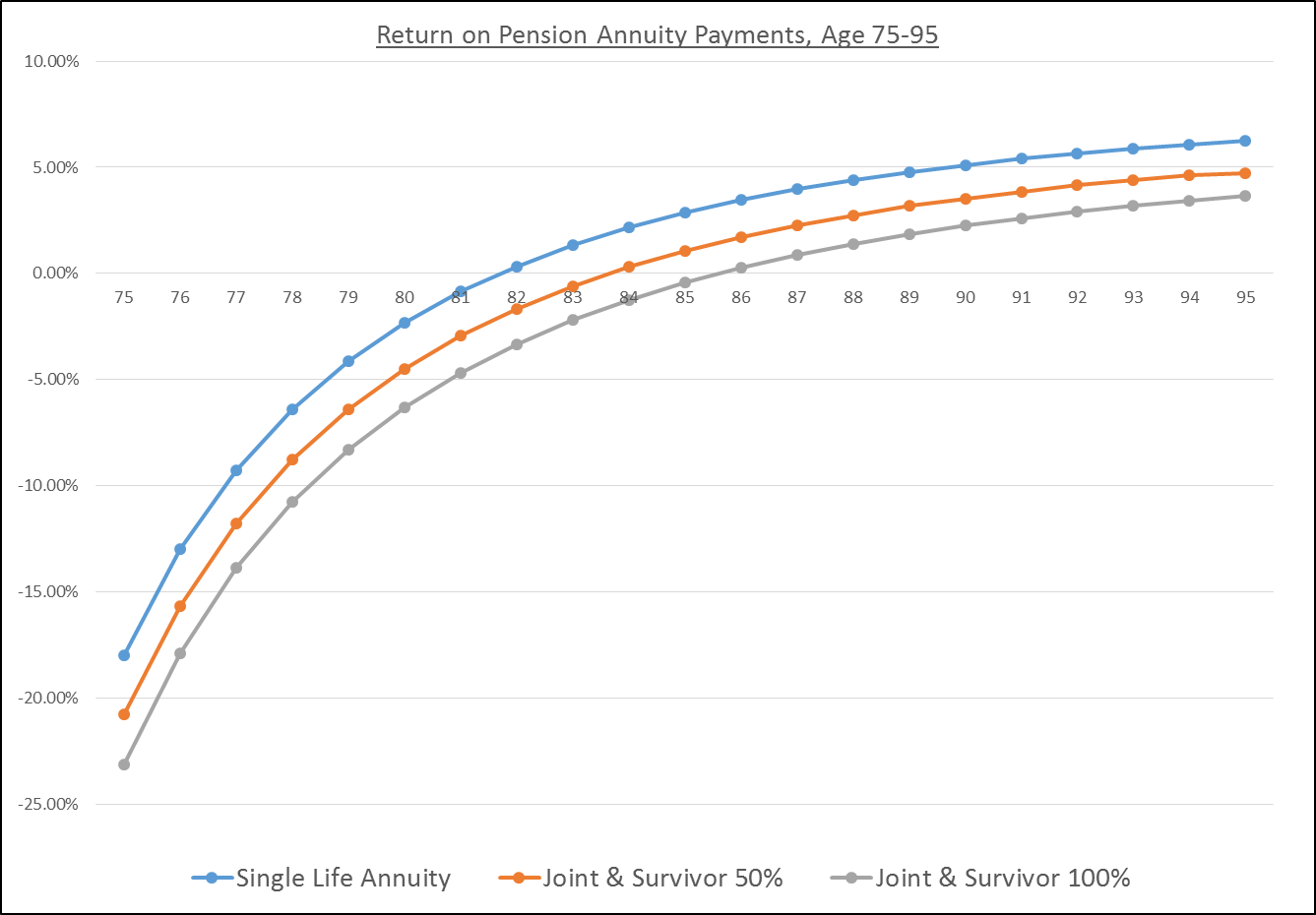

- Can you reasonably expect to outlive the “normal” life expectancy using actuarial tables? This is a good tool to evaluate this. Realizing this is impossible to answer with certainty, one can still make reasonable assumptions given lifestyle, health history, and family health history. This is a critical assessment as the Internal Rate of Return (IRR) of pension annuity payments escalates with each passing year. Conversely, the IRR is not good if the retiree were to pass away soon after electing to take the monthly payments. This dynamic is captured in the chart below which shows how the IRR improves with each passing year. So if one thinks they will live well beyond the “normal” life expectancy, the retiree could be better off with the pension payments.

Once the Dirty Harry Question is answered, retirees need to consider many other questions that could sway the decision:

- Investment Acumen: How much risk (and therefore volatility and potential return) do you need to take with a lump-sum investment to achieve a higher return than the annuity IRR over this time period? In the example above, the hurdle rate is 4%. If the hurdle rate is low, then Advantage - Lump Sum. Importantly, an investment on the lump sum should compound over time which can be a significant advantage over the pension payment.

- Inflation Adjustment: Is the monthly payment adjusted for inflation every year? This is rare, but if so, this is a big advantage as the income stream could grow every year, effectively buffering your purchasing power from the harmful effects of inflation. If “yes”: Advantage - Monthly Pension Payment.

- Survivor Benefit: Does your surviving spouse continue to get a payment after you pass away? If so, how much does it lower the baseline monthly payment amount and the future payment? Having a survivor benefit would be very positive for the pension payment but this requires some analysis on how much the payment declines relative to the single life annuity payment. Advantage – “It depends.”

- Solvency of the Pension Plan: Is there even a small chance the company/organization paying the pension could default on their payments, or will they make good on your monthly payment? This is especially critical, and for public companies can be evaluated by reviewing the funded status of the pension. If there’s even a small chance the organization defaults (or reduces the payment) that favors taking a lump sum. Advantage – “It depends.”

- Living Expenses: Are your essential living expenses already covered by other sources of income like Social Security and other income streams? If so, then you can probably afford to take a little more risk and investing the lump sum. If the pension payment would be essential to meet your basic living expenses, you may be better off avoiding the potential risks of investing. Are your living expenses already mostly covered by other sources? If “yes”: Advantage - Lump Sum.

- Legacy: Is it a goal to leave an inheritance? Taking the lump sum and investing it wisely without overspending often leaves funds available for your heirs. In most pension plans the payments stop upon your death and/or the death of your spouse. If “yes”: Advantage - Lump Sum.

- Fees: When factoring in investment returns, retirees must consider the fees associated with the pension plan and compare them to fees for the lump sum investment portfolio (fund fees, investment advisor fees, trading costs). Advantage – “It depends”

In the end, we can’t know the future, so we have to make an educated decision based on current facts and reasonable assumptions.

Once again, the big question is whether you expect to live to or beyond the “normal” life expectancy. If Dirty Harry were your wealth manager he might ask: “Do you feel lucky?”

Find more practical advice on a wide variety of wealth management topics by exploring our JIC Blog: Beyond the Numbers library.

Published 06/18/2019