Anyone who drives down a major highway these days can attest there is no shortage of billboards from banks advertising much more attractive yields on savings accounts and CDs. Obviously, the key driver for this major interest rate shift has been the Federal Reserve’s aggressive rate tightening, which they used to battle the not-so-transitory inflation over the past 18 months. With a quick online search, it’s pretty easy to find many banks offering one-year CDs paying between 4.5% and 5.0%+. In addition, money market funds at the largest custodians are currently paying between 4.5% - 5.0% depending on the amount of cash committed to the fund.

These rates seem like an attractive oasis of yield after our years of wandering in the desert with near 0% interest rates. So, at face value, it seems we’re back to the good ole days of lending banks some cash in return for healthy interest payments without having to endure the risk and volatility associated with equity and longer term fixed income investments.

What’s the Real Yield?

For many pre-retirees or current retirees, it can be tempting to consider these higher rates in the context of the “4% safe withdrawal rate” rule-of-thumb and think there’s no longer a need to endure the roller coaster ride of volatility associated with equity and (more recently) fixed income investing. If an investor needs 4% from the portfolio, why not just invest in a combination of money market and CDs?

The first problem is these rates are short term and variable. Money market rates are day to day and variable – tied to market interest rates for the shortest of fixed income securities. If the Fed were to lower rates for whatever reason, those juicy 4.5% yields would also be reduced in kind. Similarly, the shorter-term CD rates will expire when the CD matures, and if market interest rates are lower a year or two from now, those attractive rates will also no longer be available.

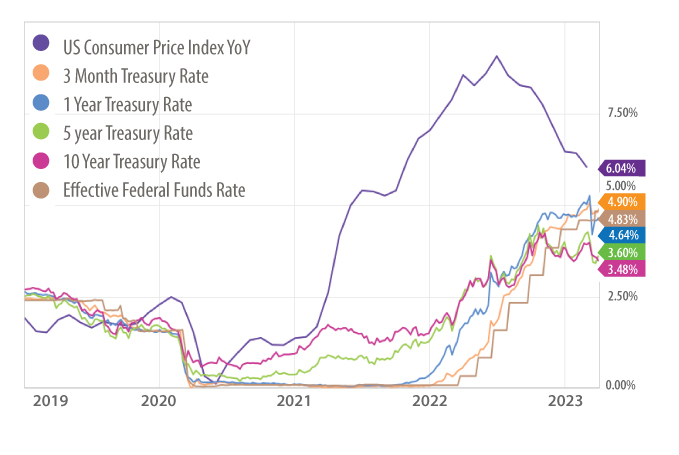

The bigger problem with this theory, of course, is that the interest rates we see on those billboards are “nominal” rates and do not factor in the deleterious effects of what are still elevated inflation rates. The chart below shows the 3-month, 1-year, 5-year, and 10-year treasury rates which are loose proxies for accompanying CD rates. (There are other differences like liquidity, FDIC insurance, etc. but we’ll keep it simple). For reference, the Fed Funds Rate is also shown. Obviously, the 6% inflation rate, even though it has retreated a bit, still dwarfs the rates being paid by US Treasuries and is still higher than the Fed Funds Rate. So, when we subtract the roughly 6% inflation, it’s clear the yield on a 1-year CD is not keeping pace with the loss in the value of those dollars if the CPI were to remain at the same level for the next 12 months. In reality, the “real rate” earned on that CD is -1% after backing out inflation.

Investment & Planning Implications

An investment strategy can have many goals, but almost always the near-term top priority is to maintain purchasing power through growth exceeding inflation, which is also known as “real” growth. If the opposite occurs and inflation outpaces growth year after year, investors may have a false sense of security when, in reality, their lifestyle is actually being eroded. In real terms, price increases on investors’ spending are rising faster than the interest income is accruing.

This is where customized and personal situations must be factored into a family’s broader wealth plan as timeframe, growth needs, risk appetite, and multi-generation goals are unique to each family. Specifically, the CPI uses a “basket of goods” that are most commonly purchased by the broad population of US citizens. Obviously, people and families in different stages of life can have dramatically different spending needs.

For example, as of February 2023, “housing” comprised 34.4% of the weight of the CPI, but if a family’s home is paid for or if they have a low fixed-rate mortgage, the “inflation” on this component really wouldn’t apply. Similarly, the cost of education is another component, but the kids could be grown and education expense is no longer a consideration. Additionally, health care is about 7% of the CPI, which is obviously more impactful for retirees.

Clearly, the composition of a family’s spending before, during, and throughout retirement is very unique to their personal situation, and planning needs to factor in personal circumstances. In designing and maintaining an asset allocation, it’s critical to keep in mind:

- The spending needs of the family in the near term and the long term, to the extent that’s possible to know.

- The asset allocation strategy must employ the core elements for balancing near-term liquidity (cash or money market reserves), growth (equities, historically the best inflation hedge), and stability (with fixed income, the ballast and buffer against inevitable stock market volatility).

Absent these foundational components of a portfolio, families risk falling behind and losing purchasing power year after year, even at lower levels of inflation than today’s rates.

Bottom Line:

It’s tempting to think today’s higher rates are a free lunch to fund a retirement lifestyle. As the inflation chart shows, nothing could be further from the truth. While the decline in purchasing power certainly isn’t as explicitly noticeable as a decline in a portfolio’s value, inflation often acts as a silent thief, robbing a family of purchasing power. There are not many guarantees with investing, but one thing is certain: a portfolio that cannot keep pace or out-pace inflation is guaranteed to impact a family’s ability to enjoy a multi-decade retirement.

Published 04/18/2023