For many of our clients, downshifting to part-time work from a full-time job after a long career is a common tactic employed to strike a healthy balance between a full-time career and full-time retirement. Many of our newer retirees tell us it’s surprisingly difficult to come to a sudden and full stop after they’ve always been employed—sometimes since before they could even drive a car! While we often suggest a period of intentional downtime to contemplate how to spend the new-found free time, it’s common among younger retirees to take on a part-time position (sometimes at their previous employer) with the intention of staying engaged with co-workers, keeping the mind sharp and having a sense of purpose. Of course, it also helps the long-term cash flow forecast to have some income to reduce the portfolio withdrawals needed to maintain the current lifestyle.

Quite often, recent retirees consider multiple options for employment and, sometimes, even consider the tradeoff of working part-time versus volunteering for a cause near and dear to their hearts. While we are not CPAs and always advise clients to consult and confirm with their tax preparer regarding the precise impact of income in retirement, we believe it to be very helpful for clients to have a general understanding of the potential after-tax “hourly rate” one is earning to evaluate this tradeoff. Retirees’ income tax profile can have many different components they never had to consider when raising their families and building careers in their younger years.

Retiree Income Considerations

For many of our retiree clients, the composition of their tax returns differs once they are no longer full-time employees. Total income no longer includes W2 wages or business income but now is comprised mostly of some mixture of taxable investment income (dividends and interest), IRA distributions, capital gains, Social Security (if claiming), pension income (if available), and maybe deferred compensation. Very often, we evaluate this income mix to integrate efficient charitable giving and potential Roth conversions. Adding wage or self-employment income to this mix can have collateral impact on many types of income that may result in an after-tax “return on income”, which may not be worth the effort and may tip the scales to foregoing the work and utilizing time and talents for different pursuits.

Using 2023 tax brackets and assuming Married Filing Jointly, these factors include:

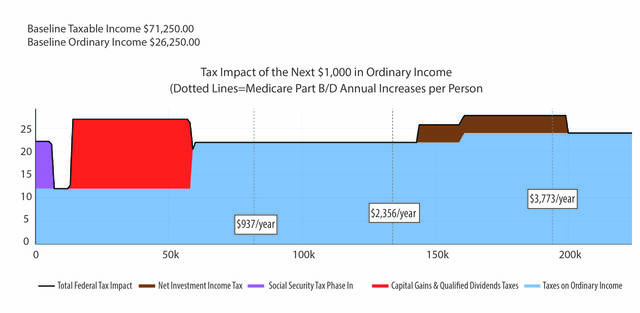

- Higher Capital Gains Tax Rates: If taxable income stays below $89,250 (MFJ), taxpayers pay 0% on capital gains income – the most attractive tax rate! Exceeding this limit by adding income would increase tax on this income to 15% (up to the high end of the bracket, $533,850).

- Increase tax on Social Security: With low income, Social Security income can avoid taxes altogether. Generally speaking, a couple with income between $32,000 and $44,000 pay tax on 50% of the benefit. A couple with income more than $44,000, may pay tax on up to 85% of their Social Security benefit.

- Social Security Earnings Limit: If a person has not reached FRA (full retirement age) and is taking Social Security benefits, the benefit is reduced $1 for every $2 they earn over $21,240. In the year one reaches FRA, the benefit is reduced $1 for every $3 of income over $56,520 (but this only applies to earnings for months prior to FRA).

- Reduction of refundable health care credits: Younger retirees who are not on Medicare usually need to purchase health care insurance on the open market. With low income, they can receive refundable credits to help offset health care premiums. However, higher income can eliminate these credits, effectively acting as a “tax” on earnings. This could also result in an unwelcome surprise tax bill because the reduced credit gets trued up when filing taxes and a retiree wouldn’t be aware of this before filing.

- Future IRMAA Medicare premiums: For those retirees who are on Medicare or approaching the claiming age of 65, having higher income can add to Medicare Part B and D premiums known as IRMAA (Income-Related Monthly Adjustment Amount), and these can be punitive. At the low end, any income over $194,000 will result in Part B monthly premiums increase to $230.80 (From $164.80) and Part D increase to $12.20 from $0. This is effectively an annual “tax increase” of $938.40.

- Roth Conversion Strategy Less Attractive: During low income years, we consult with clients and their CPAs on the strategy of adding Roth conversion income at a low rate with the intention of reducing future tax rates and/or reducing tax liabilities for heirs. With higher income from working, there is less “room” on the low end of the tax brackets for this strategy to be as impactful.

Case Study: Roger & Christina Sample

To illustrate the true tax rate for additional income, consider the case of Roger and Christina Sample, both 66 years old, retired, and taking Social Security. Before taking a job as an independent contractor for $100/hour for 10 hours a week (or about 500 hours for $50,000/year), Roger wants to know his true after-tax wage rate. Their pre-employment income is comprised of:

- $25,000 in dividend income ($20,000 qualified)

- $3,000 taxable interest, $5,000 tax-exempt interest

- $60,000 gross Social Security for both Roger and Christina, combined

- $25,000 of long-term capital gains and $3,000 of short-term capital gains

Assuming this income before extra earnings, Roger and Christina are in the 12% marginal federal bracket paying an average federal rate of 2.7%.

Adding the $50,000 in self-employment income can rapidly increase their federal tax as this increases:

- Rate on qualified dividends

- Amount of Social Security eligible for taxation

- Rate on long-term capital gains

- Payroll tax (Medicare and Social Security tax) from self-employment

All in, Roger is now paying $18,275 federal taxes on the incremental $50,000 of self-employment income or 36.5% on his income! So, his hourly rate isn’t $100/hour; it’s really $63.45/hour. Is it worth it? That’s for him and his wife to decide, but it certainly helps to evaluate of the value of one’s time in retirement.

Bottom Line

The decision to work in retirement involves much more than financial factors; staying engaged with peers, intellectual stimulation, a sense of purpose, and avoiding boredom are just a few aspects to consider. Many of our new retiree clients try to decide between working versus volunteering since these important subjective factors can also be obtained by meaningful volunteer work. This is why, evaluating the tax consequences of adding income to the tax return in retirement is critical as it clarifies the true take-home pay after factoring in so many collateral impacts to other income. For retirees, working in retirement isn’t “all about the money,” but if Uncle Sam takes a large chunk of this income, time could be better spent with a purpose other than a paycheck.

Published 12/20/2022

Johnson Investment Counsel does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.