Election Fever

We are just days away from another consequential election, and the volume of related news is reaching a fever pitch. The latest polling data, every speech, debate, town hall and tweet is instantaneously communicated to our ubiquitous screens. While this presidential election is unique for many reasons, no election in history has occurred in the context of the speed, magnitude, and hyperbole associated with our exposure to so much information. This dynamic, we fear, has provoked so many toward a myopia that this election cycle is by far the most consequential of our nation’s 244-year history. So let’s take a step back from the pinging devices and take a deeper look into what history can teach us about our investment decisions and wealth management strategies moving forward.

The Most Important Election… Ever?

Voters on both sides of the ideological aisle are claiming 2020 will be a tipping point for the future of our nation. This is certainly an important election, as they all are. And there are important issues at stake. But history is full of examples of elections that, at least in hindsight, made a lasting impact.

For example, when Jefferson was elected in 1800, there had not yet been a transfer of the presidency between political parties. Many scholars say this was the most important election not only in the history of the United States, but maybe the modern world. This set the precedent of peaceful transfer of power between parties we have enjoyed for over two centuries.

In 1828, a “westerner” from Tennessee named Andrew Jackson finally broke through to win the White House, demonstrating for the first time that a person not born of privilege could realistically set their sights on the nation’s highest office and win, as remains the case today.

And who knows what would have happened if Abraham Lincoln wasn’t elected in 1860 or 1864?

We could go on with many more examples. An enormous amount of ink has been spilled analyzing the impact of the elections of presidents (and defeats of would-be presidents). But the only sense in which we know this is the most important election ever is that it’s happening now. This doesn’t guarantee it will be the most impactful on the economy or the markets.

History is Full of Challenges and Surprises

Stock Market Performance During an Election Year: Is Near-Term Volatility Inevitable?

In today’s 24-hour news cycle it can be so easy to fall victim to the impression that markets are always more volatile around elections and the best move is to aggressively sell stocks before sharp losses ensue. But recent studies have shown that stock market returns have been higher and volatility roughly the same in election years compared to other years. Attempts to front-run volatility by timing in and out of markets are extremely risky and rarely yields any benefit. In some cases, it has led to disastrous mistakes that take years to overcome.

The Folly of Investing Based on Politics

Short-term market timing solely based on elections isn’t wise – but what about over the long term? What about the idea that “it’s different this time” and that if our preferred candidate does not win the election, our portfolios will realize sharp declines?

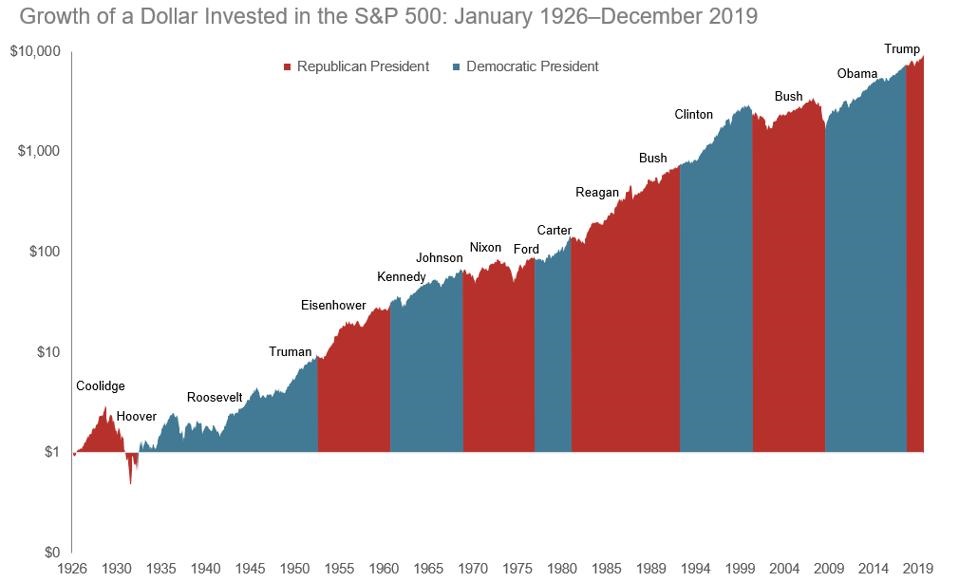

Again, applying this mindset has been a wealth-destroying strategy that could have detrimental effects on the ability to attain financial goals. As shown in the chart immediately below, if a person invested based on whether their preferred political party occupied the White House, they would have robbed themselves of the resources to reach their financial goals.

In addition, it appears markets seem to appreciate the limitations that result from opposing parties controlling the White House and Congress. In fact, since 1933, the highest returns for the S&P 500 among all “mixes” of the House of Representatives, the Senate, and the White House have been realized with a conflicting House and Senate. When this occurs, the S&P 500 has averaged a return of 13.5% annually.

In short, staying invested, regardless of which party wins the election, may ultimately be the strategy to help you achieve your long-term investment goals, such as paying for education, enjoying retirement, and more. Yes, presidential candidates may make bold promises, but the truth is none can guarantee a future. So, continue to ask yourself Why am I investing? If you're investing for a goal that's many years out, the next presidential election may not have a substantial impact on your long-term finances.

What’s Different This Time… and What’s the Same

While these history lessons may provide some comfort, we view them as guides, not rules, for the future. In working with our clients, we still critically analyze new policies and how they impact investment portfolios and our wealth planning strategies. Accordingly, we remain steadfast in our commitment to analyzing today’s crosscurrents to the markets and the economy including:

- Potential changes to income tax, corporate tax, and estate tax law

- The impact of government spending and stimulus from either party

- Federal Reserve policy with respect to accommodative interest rates

- Federal, state, and local governments reactions to coronavirus-related policies

- The timing and impact of a coronavirus vaccine

The potential impact of these and other policies span the spectrum of investing, tax planning, estate planning, and retirement cash flow planning, all of which must be considered when constructing a cohesive plan.

But while all of today’s factors will be in tomorrow’s history books, we know that over time a well-researched and balanced portfolio has successfully served as the growth engine for our clients achieving their goals. Over many decades, maintaining a healthy balance of growth-generating stocks and loss-buffering bonds has served our clients well.

So while we keep a sharp eye on this coming election, the potential changes to government policies and market impacts, we view our investment and wealth planning counsel through the lens of history. And we remain confident in the wisdom of planning for the long term.

Find more practical advice on a wide variety of wealth management topics by exploring our JIC Blog: Beyond the Numbers library.

Published 10/26/2020

Any expectations presented should not be taken as a guarantee or other assurance as to future results. Our opinions are a reflection of our best judgment at the time this presentation was created, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events or otherwise. The material contained herein is based upon proprietary information and is provided purely for reference and as such is confidential and intended solely for those to whom it was provided by Johnson Investment Counsel.